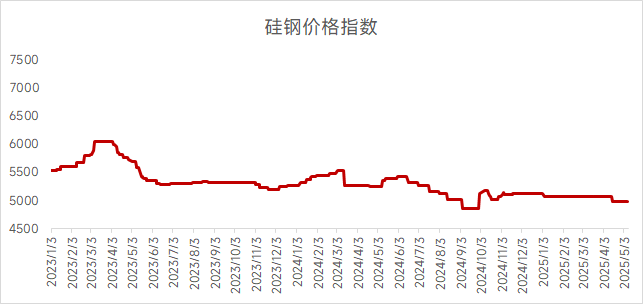

Price Dynamics of Non-Oriented Silicon Steel

Shanghai B50A800 grade: 5,050-5,100 yuan/mt

Guangzhou B50A800 grade: 4,800-4,900 yuan/mt

Wuhan 50WW800 grade: 4,800-4,900 yuan/mt

Shanghai Market:

This week, the price of cold-rolled non-oriented silicon steel in Shanghai remained in the doldrums, with some privately-owned steel mills reducing their resource prices by 50 yuan/mt. Ferrous metals futures were in the doldrums this week, and the impact of the mutual imposition of tariffs between China and the US gradually manifested, resulting in weak overall market transactions. In terms of fundamentals, Baowu's tender price has not yet been announced. State-owned enterprises' quotations barely remained stable, but some privately-owned steel mills gradually resumed production, increasing resource supply. To facilitate smooth sales, prices were slightly lowered. Downstream end-user motor users adopted a cautious stance, and the market had already entered the off-season. Coupled with the impact of China-US tariffs, purchasing strategies leaned towards conservatism, with low willingness to restock high inventory levels, and purchasing was mainly done as needed. Looking ahead, although China has agreed to negotiate with the US, both sides have adopted a tough stance. It is expected that the negotiation results will be difficult to meet market expectations. In the short term, tariff news will continue to have a negative impact. The direct export of non-oriented silicon steel and the export of downstream motor enterprises will continue to be hindered. In summary, there are signs of deterioration in market transactions after the Labour Day holiday, and the imbalance in fundamentals shows a trend of expansion. It is expected that the price of non-oriented silicon steel in Shanghai will decline slightly next week.

Wuhan Market:

This week, the spot price of cold-rolled non-oriented silicon steel in Wuhan remained in the doldrums, with average market transaction performance. Ferrous metals futures fluctuated downward, with a moderately weak market trading atmosphere and weak and stable trade quotations. In terms of fundamentals, the circulation volume of medium and low-grade resources in the market remained low. Downstream end-users mainly purchased as needed, with weak willingness to restock among end-users. Small and micro end-users generally maintained inventory at low levels. Traders actively sold off, and there was a certain room for negotiation in actual transactions. Looking ahead, the pessimistic sentiment among market participants has further intensified, with business strategies focusing on maintaining low inventory levels. In summary, it is expected that the price of non-oriented silicon steel in Wuhan will remain in the doldrums next week.

Guangzhou Market:

This week, the price of cold-rolled non-oriented silicon steel in Guangzhou maintained a weak and stable pattern, with a decline in market transaction activity after the Labour Day holiday. In terms of fundamentals, affected by the decline in apparent demand for finished steel products, futures fluctuated downward, leading to a slight decrease in spot steel prices. Traders were generally pessimistic, with a moderately weak overall trading atmosphere and a reduction in spot transactions. Looking ahead, the negative impact of tariffs is still fermenting, having a bearish impact on the export of downstream industries such as home appliances and motors. The market sentiment is characterized by a wait-and-see approach.In summary, it is expected that the price of non-oriented silicon steel in Guangzhou will undergo a narrow adjustment next week, with a slight price reduction anticipated for some grades of resources.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)